Athene: Case Study in Private Credit, Insurance and Ratings Run Amok

Article

research

Published: 06/14/2025

Read Time: 4 min

0:00

I recently published an article on Athene highlighting risks which implicated ratings and ratings agencies. Yesterday, the WSJ published a story raising questions on private credit ratings which perfectly illustrated the issues I raised.

Below is a summary of these risks:

Private Credit and Ratings Shopping

While all debt instruments are at risk for rating shopping, the risk is greater for private credit as they operate in the shadows, are often not public and need one rating. The NAIC requires one rating for risk-based capital.

In Athene’s case, Apollo is both asset originator and Athene’s asset manager, which increases the incentives and ease of rating shopping. In my analysis 50% of Athene’s purchases had an Apollo affiliation - mostly private credit.

According to the SEC’s Office of Credit Ratings, Egan Jones (EJR) and KBRA issue most private credit ratings. It’s worth questioning how minor rating agencies dominate private ratings - easier standards are an obvious culprit.

The WSJ focused on EJR and highlighted whistle blower lawsuits alleging an improper ratings process.

EJR rates around 21K CUSIPs which appears far beyond what would seem possible given the size of their staff (around 20). By comparison, Fitch rates 21K entities with 1133 analysts. Though these aren’t exactly apples-to-apples, it does raise the concern that EJRs rating process emphasizes profitability over quality.

Post financial crisis, ratings regulation is worse, not better. Private Credit, and the increase in # of rating agencies amplify systemic credit risk.

Apollo and Athene – Conflicts of interest and ratings

Apollo’s ownership of Athene and role as Athene asset manager poses significant conflicts of interest. In my article I highlighted 3 large Apollo affiliated Athene investments that comprised more than 50% of capital - all privately rated. Apollo as originator can shop for the single best rating to maximize Athene’s capital.

The largest conflict relates to Athene's purchase of $4B debt in an Intel Chip fabrication business, where Apollo negotiated an $11B purchase. Without Athene's balance sheet this deal doesn't get done.

Flawed Ratings of Athene

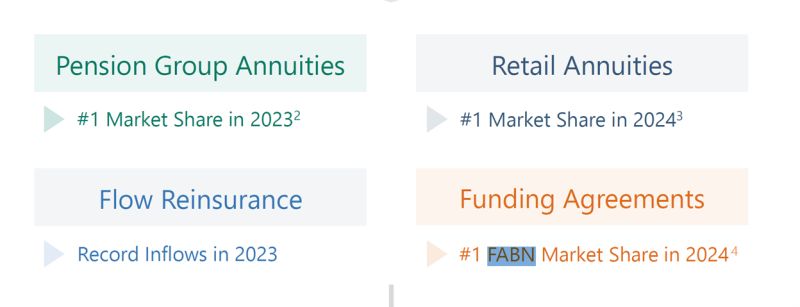

1) Moody’s awards Athene a AA for the market share component of their rating. This is backwards. Athene’s market share is DIRECTLY a function of asset risk as higher yielding assets enables them to compete better in the annuity and other liability markets (see image).

2) Flawed Asset Risk analysis: RAs rely on ratings assigned by other RAs. Hence Moody’s will accept KBRA, EJR, etc, ratings. If Athene’s investment ratings are inflated, Athene’s own Single-A rating will be inflated.

3) Reliance on Apollo: Moody’s elevates Athene’s credit rating for the financial flexibility component from BB to A based on the false notion that Apollo is a source of strength - Apollo argues the opposite.